What is Correspondent Banking?

I find myself fielding a lot of questions from clients about “correspondent banks” and the purpose they serve in international financial markets, plus the role they play in delivering an international payment from a payor in one country to a payee in another country. Having been in FX and payments my entire career, which spans 3 decades (yikes), I sometimes take for granted all the nuances associated with cross-border payments.

First, let’s take a look at the definition of “Correspondent Bank”. From Investopedia:

The term correspondent bank refers to a financial institution that provides services to another one—usually in another country. It acts as an intermediary or agent, facilitating wire transfers, conducting business transactions, accepting deposits, and gathering documents on behalf of another bank. Correspondent banks are most likely to be used by domestic banks to service transactions that either originate or are completed in foreign countries. Domestic banks generally use correspondent banks to gain access to foreign financial markets and to serve international clients without having to open branches abroad.

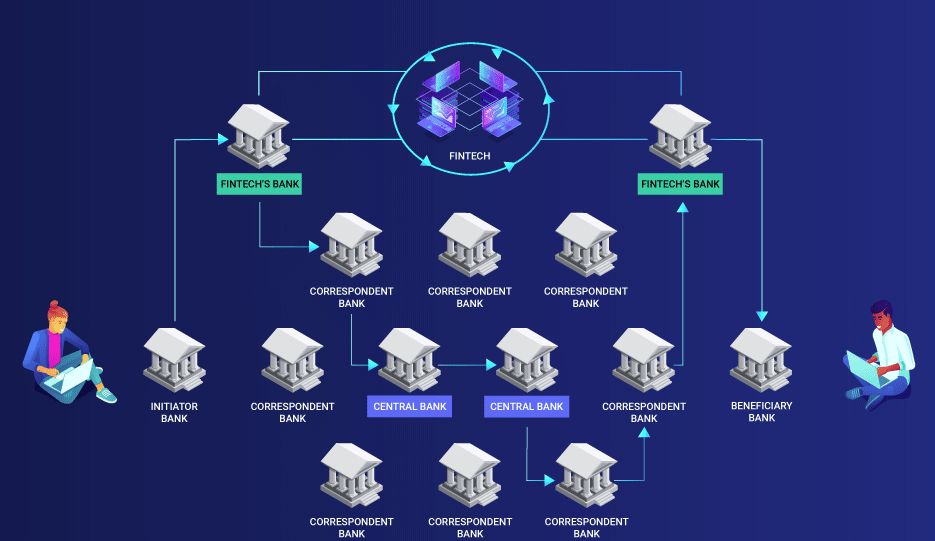

In simpler terms, correspondent banking is a service that account holders from one bank in a specific jurisdiction (respondent) can utilize the services from another bank in a different jurisdiction (correspondent). For the purpose of this post, the services essentially enable a bank to provide cross-border payments to its customers in countries in which it does not have a physical presence.

For example:

- US Payor orders a cross-border payment using a local/regional community bank to deliver funds electronically to a UK Payee.

- US community bank, using SWIFT, sends instructions to a correspondent bank that has a bank relationship with the beneficiary’s bank in the UK to deposit the equivalent GBP into the payee account.

- Beneficiary bank deposits the GBP into the payee account as instructed.

Steps 1-3 are pretty straightforward, but it takes about 2 business days to complete. In addition, the Payor is paying a fee to her community bank for the service. The correspondent bank will trim an amount from the payment as a fee to cover correspondent bank services. In addition, the beneficiary bank will trim a bit more to cover the cost of accepting the payment and depositing it into the payee account. Finally, there’s the foreign exchange that is executed to convert the original USD amount into the final GBP amount. The community bank may or may not be able to provide the payee with a conversation rate, which leaves the correspondent bank or the beneficiary bank to convert the funds into usable GBP. Unfortunately, no one will know which bank will execute the foreign exchange or what kind of rate will be applied to the conversion.

The cons:

- Payment takes up to 2 business days to complete

- Hefty wire fee paid up front

- Correspondent bank fee

- Beneficiary bank fee

- Unsure of exchange rate

The pros:

- Traceable

- From SWIFT, you can retrieve an MT103, which can be used as proof of payment

- The delivered funds are considered “good funds”, which means that the payee can use the money immediately

- Cross-border payments using SWIFT is a tested and reliable method to send an international payment

Luckily at Routefusion, we have taken care of the correspondent banking cons and provided our customers with a seamless way to move money around the world.

We love to educate companies and individuals of all sizes and walks of life about the cross-border payments space. If you have any questions please do not hesitate to reach out!

Email: info@routefusion.com

Schedule a consult: https://routefusion.com/contact

☮️ & 💕 - Routefusion

-- Photo Credit to Bitpay :)