What are local payments and why should I use them?

Local Payments what does this mean and how does it affect your product and customers when deciding on your embedded cross-border payments solution?

Local Payments

Local payments have many names. They are also referred to as, International ACH, local payouts, borderless transfers, low-value payments, real-time payments, etc. At Routefusion we use the terminology local payment because we think it's the least confusing.

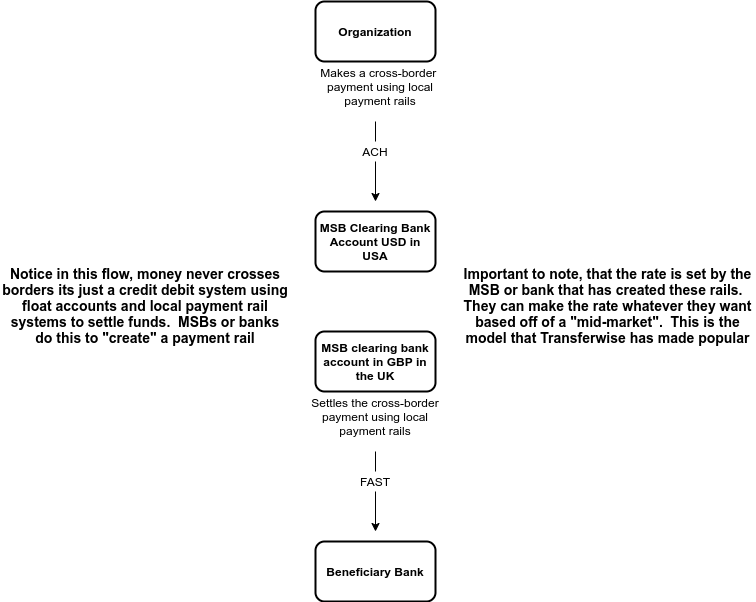

A local payment is simply a payment that is made using the local payment rails in a given country. What does that mean? It means that if I make a cross-border payment in the USA (or any country for that matter) to the UK (or any country) and I choose to send it over local payment rails, the funds will be collected via local payment rails of the country I am sending from, in this case, ACH, and then it will be paid out from a float bank account in the UK using the local payment rails there, such as FPS or SEPA.

If that sounds confusing, check out the below workflow, which should help clarify further.

Local payments are great but also have some drawbacks. Below is a list of the pros and cons of local payments.

Pros

More cost effective

- Because companies are not actually using liquidity in FX markets, they can set their own rates based off of a mid-market rate. If you are curious you could subscribe to service like fixer.io to find the mid market rate and then mark it up .5%, etc.

Much faster than SWIFT

- Since the payments are traversing real time local payment networks like FPS, SPEI, or SEPA, etc, payments can arrive at the destination "instantly". This is what real-time cross-border payment companies are doing (ill do a better write up on this later).

Cons

No automated or widely recognized receipt of transmission

- If you are doing large B2B transactions over the SWIFT network, you get a receipt of sorts called an MT103. The MT103 is as good as gold if presented to any bank. It is widely recognized that the money has been sent over the SWIFT network and that it will arrive. This is great because it greatly reduces the chances of fraud in the industry. The receiving party cannot say they did not receive the payment if the MT103 exists, because the MT103 says that no matter what they WILL receive the payment. If you do local payments, the MT103 does not exist. You can be provided a receipt of transmission from the bank or the MSB, BUT this does not mean that the receiving bank will honor it, and leaves the sender at an increased risk of fraud.

Why Should I use Local Payments

This is a question that you must answer for yourself and your product. At Routefusion we typically advise the below.

If you are a payroll provider that is doing frequent smaller payouts and you have a good fraud team or policies, then local payments make the most sense. If you are doing intra-company transfers, local payments make the most sense. If you are enabling large b2b transactions where the supplier is a 3rd party, we recommend not using local payments and using SWIFT payments. At the end of the day it all comes down to how well do you understand your customers, and how much risk are you willing to take? Local payments are the most efficient and fastest way of sending payments today, but they can open you and your customers up to fraud. The alternative is SWIFT payments (article coming soon), but they can take alot longer, and are generally more expensive, but the fraud rate goes down dramatically.

Here at Routefusion, we Love local payments, but even more we LOVE making our customers happy and helping then solve their complex payout and receivables problems. We are always happy to discuss more about your needs and answer any questions you may have about the very esoteric world of cross-border payments.

Email: info@routefusion.com

Schedule a consult: https://routefusion.com/contact

☮️ & 💕 - Routefusion